![]()

本日更新の2026年02月試験エンジンとPDF LLQPテスト無料!

究極のガイド準備LLQP正確なPDF解答

IFSE Institute LLQP 認定試験の出題範囲:

| トピック | 出題範囲 |

|---|---|

| トピック 1 |

|

| トピック 2 |

|

| トピック 3 |

|

| トピック 4 |

|

質問 # 81

Kevin owns a construction business and wants to take out accident and sickness insurance to protect his income in the event of disability. On his application form, he indicated that he had competed in motocross races over the past five years. What requirements does Kevin need to comply with before the insurer can issue the policy?

- A. Kevin only needs to specify how often he engages in the sporting activity.

- B. Kevin needs to complete a special questionnaire, as well as specify how often he engages or intends to engage in the sporting activity in the future.

- C. Kevin needs to complete a special questionnaire as well as specify how often he engages or intends to engage in the sporting activity in the future; thus, an exclusion rider may be required by the insurer.

- D. Kevin only needs to answer the medical questions.

正解:C

解説:

Comprehensive and Detailed Explanation:

Motocross is high-risk, requiring a detailed questionnaire and frequency disclosure. Insurers may impose an exclusion rider (Chapter 7:Insurance Recommendation, Contract, and Service Needs).

Option A: Incorrect; misses activity risk.

Option B: Incomplete; lacks detail.

Option C: Incomplete; misses exclusion possibility.

Option D: Correct; full process with potential rider.

Reference: LLQP Accident and Sickness Insurance Manual, Chapter 7:Insurance Recommendation, Contract, and Service Needs.

質問 # 82

Nathalie worked for 25 years as an administrative assistant at a manufacturing company. When she left the company 10 years ago, she transferred the money that she accumulated from the company's pension plan into a locked-in retirement account (LIRA). Now she is 60 years of age and would like to withdraw the money from the LIRA.

Under which of the following circumstances would Nathalie be allowed to withdraw her funds?

- A. She will start collecting QPP benefits.

- B. She is retiring.

- C. She is disabled and her life expectancy is reduced.

- D. She moved to Arizona last year.

正解:C

解説:

Locked-In Retirement Accounts (LIRAs) are subject to specific restrictions regarding when and how funds can be accessed. Under LLQP regulations, individuals can generally only withdraw funds from a LIRA before retirement under certain circumstances. These include:

* Disability and a reduced life expectancy, as defined by the plan's requirements, which allow for early withdrawal due to significant financial or health hardships.

In contrast:

* Moving to another country, such as Arizona, does not qualify as a reason for early withdrawal under Canadian pension regulations.

* Retirement alone, without converting the LIRA into a Life Income Fund (LIF) or similar product, does not directly permit withdrawals from the LIRA.

* Collecting QPP benefits does not impact the withdrawal conditions of a LIRA directly unless combined with an allowable reason such as disability with reduced life expectancy.

Thus, option B correctly reflects the LLQP criteria under which Nathalie may access her LIRA funds early due to disability and a shortened life expectancy.

質問 # 83

Jessica is 61 years old and has $460,000 invested in a registered retirement savings plan (RRSP). She is retiring due to health issues that are expected to reduce her life expectancy and will prevent her from working until she is 65. She would like to transfer her RRSP funds into an annuity that will pay her monthly benefits for the rest of her life.

Which of the following annuities is the BEST option for her to purchase?

- A. Life annuity.

- B. Life annuity with a 20-year guaranteed period.

- C. Term annuity to age 90.

- D. Impaired life annuity.

正解:D

解説:

Due to Jessica's reduced life expectancy, an impaired life annuity would provide higher monthlypayments than a standard life annuity. This type of annuity takes her medical condition into account, offering larger payouts based on a shorter expected payment period. LLQP resources recommend impaired life annuities for individuals with significant health issues, as these provide better income compared to other types.

Options A and C offer a fixed period but don't maximize monthly income for someone with a reduced life expectancy. Option B would provide a standard income for life but not the potentially enhanced income from an impaired annuity.

質問 # 84

Rhonda is a sixty-year-old biologist at the local university. She has two adult children Connor and Daniel. She meets her life insurance agent Todd to make sure that if something were to happen to her that everything would be taken care of. She has taken the initiative to have a will done that has all of her assets divided between her two children after any debts or taxes are settled. She knows her boys are not great with money so she names her friend Sandra as the executor.

One of the things that Rhonda is concerned about is the taxes that will be owed on her final tax return and thinks a life insurance policy would be a good idea to solve her issue.

What should Todd recommend while completing a life insurance policy to make sure that Rhonda's concerns are met?

- A. Name her estate as the beneficiary

- B. Name Connor and Daniel beneficiaries with Sandra as a trustee.

- C. Name Sandra as the beneficiary and have her distribute the funds to Connor and Daniel.

- D. Name Connor and Daniel beneficiaries with her estate as a contingent beneficiary.

正解:A

解説:

Comprehensive and Detailed Explanation From Exact Extract:

If Rhonda wants the policy to be used for paying taxes on her estate, naming theestateas the beneficiary is the most appropriate option. The LLQP notes that naming the estate allows the proceeds to directly addressestate liabilities, such as taxes, before distribution to heirs.

質問 # 85

Antonin and Magali are common-law partners in their thirties. They have two children together: a five-year- old daughter and a two-year-old son. Divorced from ex-wife Vanina, Antonin must pay her $1,500 a month in child support until their 10-year-old son reaches 25 years of age. Antonin is covered under a group life insurance policy equal to one year of his $75,000 annual salary. Magali does not currently earn any income, as she takes care of their two children full-time. Antonin is the sole owner of their residence, which will be fully paid off in 25 years.

What life insurance coverage do Antonin and Magali need in their situation?

- A. Permanent coverage to replace Antonin's income.

- B. Mortgage payment coverage, group insurance coverage equal to twice Antonin's annual salary and 15- year term coverage to support the child from his previous relationship.

- C. Mortgage payment coverage, term-to-age 65 coverage to replace Antonin's income and 15-year term coverage to support the child from his previous relationship.

- D. Permanent coverage to replace Antonin's income and 15-year term coverage to support the child from his previous relationship.

正解:C

解説:

Comprehensive and Detailed Explanation From Exact Extract:

This is a multi-need situation. The LLQP recommends layering coverage:

* A 25-year term policy for mortgage protection.

* A term-to-65 policy for income replacement.

Reference: Insurance Study Guides Chinese.pdf, Needs Analysis - Family and Legal Obligations

質問 # 86

Josh is an established advisor who specializes in group benefits. He recently hired Bryan as a marketing manager. Bryan will be responsible for advertising and creating a social media platform for Josh's company.

Among other things, Bryan is developing a monthly electronic newsletter, which he plans to email to potential and existing clients. However, because this is a brand new initiative, none of the would-be recipients has subscribed to the newsletter or asked to receive any such communication from Josh's company. What law should Josh and Bryan be mindful of before sending their newsletter?

- A. The Personal Information Protection and Electronic Documents Act.

- B. The Canadian Anti-Spam Legislation.

- C. The rules governing the National Do Not Call List.

- D. The Privacy Act.

正解:B

解説:

Comprehensive and Detailed in Depth Explanation with Exact Extract from Documents and Guides:

TheCanadian Anti-Spam Legislation (CASL)governs the sending of commercial electronic messages (CEMs), such as emails or newsletters, to recipients in Canada. According to CASL, businesses must obtain consent- either express or implied-before sending CEMs to individuals. Since Bryan's newsletter is a new initiative and none of the recipients have subscribed or requested it, Josh and Bryan lack consent, making CASL the primary law they must comply with. TheIFSE Ethics and Professional Practice Course (Common Law) highlights CASL under ethical businesspractices, noting that non-compliance can result in significant penalties. The Personal Information Protection and Electronic Documents Act (PIPEDA) deals with the collection and use of personal information, not unsolicited messages specifically. The Privacy Act applies to federal government institutions, and the National Do Not Call List pertains to telemarketing calls, not emails.

Thus, option B is correct.

References:

IFSE Ethics and Professional Practice Course (Common Law), Module 4: Regulatory Environment, Section on "Canadian Anti-Spam Legislation (CASL)."

質問 # 87

Maeve is an Ontario resident. Fifteen years ago, she purchased a $250,000 whole life insurance policy and named her husband Guillaume as the primary beneficiary and her 4-year-old son Edwin as the contingent beneficiary. Last week, Tasha, Maeve's insurance agent called her to ask if she has had any life changes that would warrant a meeting to review her insurance coverage. Maeve informs her that over the last year she divorced Guillaume and that she is now living with her new boyfriend Eduardo. Tasha asks to meet Maeve to review her beneficiary designation. Who will receive Maeve's death benefit if she dies today?

- A. Edwin

- B. Eduardo

- C. Maeve's estate

- D. Guillaume

正解:D

解説:

In Ontario, unless a beneficiary designation is changed formally through the policyholder or as part of a court order, the originally designated beneficiary remains entitled to the death benefit. Since Maeve has not updated her beneficiary designation following her divorce, Guillaume remains the primary beneficiary. Divorce does not automatically revoke a beneficiary designation in life insurance policies. Therefore, if Maeve dies today, Guillaumewould receive the death benefit. Edwin, the contingent beneficiary, would only receive the benefit if Guillaume were unable to (e.g., predeceased).

質問 # 88

(Kara's uncle recently passed away, leaving her an inheritance. Since Kara does not hold any investment account and is not sure what to do with this unexpected influx of money, her cousin referred her to his own financial advisor.

What information should the advisor first seek to obtain from Kara to begin developing an investment strategy that meets her needs?)

- A. Who Kara wants to list as beneficiary.

- B. The rate of return Kara wants for her investment.

- C. Whether Kara would like to duplicate what her cousin has.

- D. How liquid Kara needs her investment to be.

正解:D

解説:

To create an appropriate investment strategy, the advisor must understand Kara'sliquidity needs- how easily and quickly she might need to access her money without significant loss. Liquidity considerations are fundamental when setting up an investment plan, especially for someone without prior investments and an uncertain timeline for using the funds.

Exact Extract:

"Liquidity refers to the ability to access funds readily and should always be assessed in determining appropriate investment recommendations." (Reference:Segfunds-E313-2020-12-7ED, Chapter 1.1.2.5 Liquidity)

質問 # 89

Lily works for Cloud 9 Inc. She earned $120,000 in Year 1 and $125,000 in Year 2. Lily contributes 5% of her income into a defined contribution pension plan (DCPP), and this contribution is matched by the employer. Lily has unused contribution room of $15,000 andwants to know how much she can contribute to her registered retirement savings plan (RRSP) in Year 2.

- A. $25,000

- B. $24,600

- C. $31,250

- D. $30,600

正解:B

解説:

Lily's RRSP contribution room is reduced by her DCPP contributions. Her total income for Year 2 was

$125,000, and she contributed 5% ($6,250) to the DCPP, matched by the employer, for a total of $12,500.

The Pension Adjustment (PA) for her DCPP contribution would be $12,500, which reduces her RRSP contribution room.

Calculation:

RRSP limit based on previous year's income (18% of $120,000): $21,600

PA reduction: $12,500

Remaining RRSP contribution room for Year 2: $21,600 - $12,500 = $9,100 Including her unused contribution room: $9,100 + $15,000 = $24,100 So, Lily can contribute $24,600 to her RRSP in Year 2.

質問 # 90

Dennis, aged 56, is an actuary. He owns both a disability insurance policy and a renewable term life insurance policy. His life insurance policy includes a supplementary benefit: the waiver of premium for total disability benefit. Following a motorcycle accident, Dennis suffers a traumatic brain injury. His disability benefits begin after the waiting period. While receiving those benefits, his term life insurance policy comes up for renewal.

How will the supplementary benefit included in that policy help Dennis?

- A. It will increase the amount Dennis receives as a disability benefit.

- B. It will pay his life insurance premiums before and after the policy's renewal, so long as he is disabled.

- C. It will pay his life insurance premiums up until the policy's renewal, but not after.

- D. It will pay the premiums for the disability insurance.

正解:B

解説:

Comprehensive and Detailed Explanation From Exact Extract:

TheWaiver of Premiumrider ensures that while the insured remains disabled, the life insurancepolicy premiums are paideven beyond renewals(subject to policy terms). This prevents policy lapse and maintains coverage. LLQP confirms that the waiver continues during verified disability status regardless of term renewals.

Reference: Insurance Study Guides Chinese.pdf, Waiver of Premium Rider - Ongoing Coverage

質問 # 91

(Matthew, 40 years old, is leaving his employer (XYZ Corp) and has $100,000 in a group RRSP.

What should Shawn, the advisor, do?)

- A. Arrange for the transfer of the cash value of Matthew's group RRSP to the group TFSA.

- B. Calculate the commuted value of Matthew's group RRSP account and arrange transfer to the DPSP.

- C. Provide Matthew with forms to transfer his group RRSP holdings to an individual RRSP.

- D. Arrange for the transfer of Matthew's group RRSP to his wife's group RRSP.

正解:C

解説:

Upon termination of employment, employees cantransfer group RRSP funds to an individual RRSPto maintain tax-deferred growth without triggering a taxable event.

Exact Extract:

"Upon leaving employment, a member may transfer their group RRSP assets to an individual RRSP to maintain tax deferral." (Reference:Segfunds-E313-2020-12-7ED, Chapter 1.3.11.2 Group Plans#45:5†Segfunds-E313-2020-12-7ED.

pdf**)

質問 # 92

John purchased a permanent life insurance policy for his grandson, Richard, when Richard was born 28 years ago. This policy has increased in death benefit over time and holds sizeable cash value. Now that Richard is older, John would like to transfer this policy to him as he now is working and has a family.

What does John need to know about this transfer in relation to tax implication?

- A. John should roll this policy over to Richard's father first, then Richard's father should roll it over to Richard without tax implication.

- B. John is not responsible for any disposition triggered by Richard as they will be taxable to Richard only.

- C. The transfer will be done with tax implication as Richard isn't his child.

- D. The transfer will be done when Richard pays consideration to John for fair market value of the policy.

正解:A

解説:

Comprehensive and Detailed Explanation From Exact Extract:

In Canada, the transfer of a life insurance policy from agrandparent to a grandchildisnot tax-deferred.

However, transferring first to theparent (John's child)and then from parent to Richard qualifies as atax-free rolloverunder the Income Tax Act, as the child-parent-grandchild chain preserves tax deferral. LLQP outlines this indirect transfer as a compliant tax strategy.

Reference: Insurance Study Guides Chinese.pdf, Policy Ownership Transfer and Taxation - Multi- Generation Transfers

質問 # 93

Rene, age 39, is a framing carpenter at a company that builds doors and windows. He has group disability insurance equivalent to 60% of his annual salary, which is $70,000. His monthly living expenses are $3,500.

Since he has no pension plan at work, Rene has enrolled in an individual RRSP through payroll deductions ($1,000 per month). His RRSP savings currently amount to $45,000. In addition, Rene has $10,000 in a non- registered savings account. What should Rene's life insurance agent advise him?

- A. Rene should, in addition, buy $1,000 per month of individual disability insurance, given his RRSP commitment.

- B. Rene is already sufficiently protected through his group disability insurance and his RRSP.

- C. Rene should, in addition, buy individual disability insurance covering 40% of his salary for unexpected expenses.

- D. Rene is already sufficiently protected through his group disability insurance.

正解:C

解説:

Comprehensive and Detailed Explanation:

Rene's salary is $70,000/year, and his group disability insurance provides 60% of this, or $42,000/year ($70,000 × 0.60), equating to $3,500/month ($42,000 ÷ 12). His monthly expenses are $3,500, so this just covers his needs if disabled. However, the LLQP stresses considering unexpected expenses (e.g., medical costs, inflation) beyond basic living expenses (Chapter 2:Insurance to Protect Income).

RRSP contribution: $1,000/month, savings: $45,000 (registered) + $10,000 (non-registered).

40% of salary = $70,000 × 0.40 = $28,000/year or $2,333/month.

Option A: Incorrect; $3,500/month matches expenses but leaves no buffer for unforeseen costs.

Option B: Incorrect; RRSPs are for retirement, not disability liquidity, and don't enhanceimmediate protection.

Option C: $1,000/month additional coverage is arbitrary and insufficient for 40% of salary; it doesn't align with needs analysis.

Option D: Correct; 40% of salary ($2,333/month) on top of $3,500 provides $5,833/month, offering a safety net for unexpected expenses, consistent with LLQP's holistic protection approach (Chapter 6:Client Profile).

Reference: LLQP Accident and Sickness Insurance Manual, Chapter 2:Insurance to Protect Income, Chapter 6:

Client Profile.

質問 # 94

Luisa owns a balanced segregated fund currently valued at $50,000. Her mother Linda is the current revocable beneficiary of the policy. However, Luisa has been dating Benjamin for a year and would like to name him as the new beneficiary of her policy.

Which of the following statements about modifying the beneficiary designation is CORRECT?

- A. Luisa can call the insurer's head office to notify them of the change.

- B. Luisa can modify the designation anytime.

- C. The change will take effect on the date that the insurer receives the change of beneficiary form.

- D. Since Linda is Luisa's named beneficiary, she would need to consent to the change.

正解:C

解説:

Beneficiary changes in insurance contracts generally become effective once the insurer receives and processes the signed change form. This is supported by LLQP material, which specifies that changes to beneficiary designations must be documented and received by the insurer for the new designation to take effect. Since Linda is a revocable beneficiary, Luisa can make this change without requiring Linda's consent.

Option B is incorrect as revocable beneficiaries do not require consent for changes. Option C is too general, and D is incorrect because a formal written change form is typically required.

質問 # 95

Six years ago, when Kacey was working as an active firefighter, she purchased a $200,000 30-year term life insurance policy. At the time, the insurance company rated her policy. Recently, she changed roles and now works for the fire department's public relations office, answering media calls and filling out paperwork. She meets with her insurance agent, Bernice, to ask if the insurer would consider reducing her premiums.

- A. The insurer cannot reduce the premium, but Kacey can apply for a new policy at a lower premium.

- B. The premiums cannot be increased once the policy is issued.

- C. The premiums can be reduced only if the policy has been in force for more than two years.

- D. Her premiums can be reduced since she is no longer a firefighter.

正解:A

解説:

When a term life insurance policy is issued with a specific rating based on risk factors, such as Kacey's former occupation as a firefighter, the premiums are generally fixed and non-negotiable post-issuance.

However, Kacey can apply for a new policy, which would consider her current lower-risk occupation and potentially offer lower premiums. She would need to undergo underwriting again. Thus,Option Bis correct, as the existing policy's premiums cannot be adjusted retroactively to account for her new role.

質問 # 96

Jasper is the sole breadwinner in his family. His wife Stephanie has chosen to dedicate all of her time to raising their 3 young children. Luckily, Jasper earns a monthly after-tax income of $25,000 working as a family doctor in the local clinic. Jasper meets with his insurance agent Odda to purchase a life insurance policy that will ensure his family will be able to continue toenjoy their current lifestyle in the event of his death. If his average tax rate is 40% and the investment return is 4%, how much life insurance should Jasper purchase based on the income replacement approach?

- A. $1,041,666

- B. $625,000

- C. $7,500,000

- D. $12,500,000

正解:D

解説:

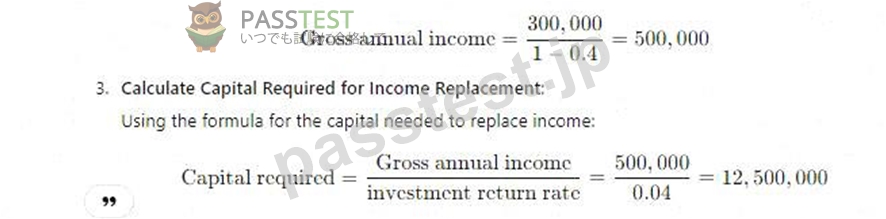

The income replacement approach calculates the amount of life insurance needed to replace Jasper'safter-tax income for his dependents over a given period, accounting for an investment return. To maintain the family's current lifestyle, we need to determine the capital required to generate a monthly after-tax income of $25,000.

Calculate the Annual Income Needed:Monthly income required: $25,000Annual income required: $25,000 ×

12 = $300,000

Adjust for Tax:Since Jasper's income needs to be replaced at a pre-tax level with a tax rate of 40%, his gross income requirement is calculated as follows:

A close-up of a math Description automatically generated

Thus, Jasper needs a life insurance policy worth$12,500,000to replace his income, allowing his family to maintain their lifestyle with a 4% investment return. This calculation aligns with LLQP principles, ensuring that the income replacement fully addresses both current lifestyle needs and tax implications.

質問 # 97

After working nine years as an insurance agent, Jamie decides to make a change in her life and go back to school. A colleague she used to work with on personal health insurance congratulatesher and tells her that he will pay her a flat fee for every health insurance referral she makes to him, as long as the referral results in a sale. What could be said about this referral arrangement?

- A. It is allowed, because Jamie used to be a licensed agent herself.

- B. It is allowed, provided the persons being referred are aware of the arrangement.

- C. It is not allowed, because Jamie earns a flat fee for each prospect referred.

- D. It is not allowed, because Jamie's earnings are contingent upon the agent's sales.

正解:D

解説:

Comprehensive and Detailed in Depth Explanation with Exact Extract from Documents andGuides:

TheIFSE Ethics and Professional Practice Course (Common Law)states that only licensed agents can receive compensation for insurance referrals, and payments contingent on sales are prohibited for unlicensed individuals. Jamie is no longer an agent, and the flat fee is contingent on sales, violating regulatory rules. Her past licensure (A) doesn't permit this, client awareness (B) doesn't override the licensing requirement, and the flat fee structure (D) isn't the issue-contingency is. This protects against unlicensed solicitation, making C correct.

References:

IFSE Ethics and Professional Practice Course (Common Law), Module 4: Regulatory Environment, Section on "Compensation and Referrals."

質問 # 98

Harper owns a disability insurance policy that will pay her a monthly benefit if she becomes unable to work.

At the time she applied for the policy, Harper was a new graduate with an annual income of $60,000, and she qualified for a monthly benefit of $3,000. Instead of taking the maximum benefit, she focused on paying off her student loans and keeping her insurance premiums low. She elected to purchase a monthly benefit of

$2,500 and add the future purchase option (FPO) rider for up to $500 a month of additional coverage. Now she is further along in her career, Harper earns $100,000 a year, and she meets with her insurance agent Trish to increase her coverage. Harper would like her new monthly benefit to be $5,000.

Which of the following statements about Harper's coverage is TRUE?

- A. Harper can exercise the FPO and increase her monthly benefit by $2,500.

- B. Harper cannot apply to receive an additional $2,000 of coverage, but she can exercise the FPO and increase her monthly benefit by $500.

- C. If Harper wants to increase her coverage, she will have to apply for an additional $2,500 of monthly benefit with full medical underwriting.

- D. Harper can exercise the FPO, increase her monthly benefit by $500, and apply for an additional $2,000 of monthly benefit with full medical underwriting.

正解:D

解説:

Harper has aFuture Purchase Option (FPO)rider on her disability insurance policy, which allows her to increase her coverage by a predetermined amount (in this case, $500) without undergoing additional medical underwriting, provided she exercises this option at specific intervals. Given her increased income, Harper wishes to increase her monthly benefit to $5,000. By exercising the FPO, she can automatically add $500 to her current benefit, raising it from $2,500 to $3,000 without medical underwriting. To reach her desired benefit of $5,000, she would need an additional $2,000. For this portion, she would need to go through medical underwriting as it exceeds the FPO amount. Thus, option D is correct, as it accurately reflects the process and options available to Harper under the LLQP guidelines for utilizing the FPO rider along with additional underwriting for further increases.

質問 # 99

Surjit and Rajbir got married in 2010, and Surjit named Rajbir as the irrevocable beneficiary of his life insurance contract. In 2017, the couple divorced amicably, and Surjit met with his insurance representative, Ivan, to review his plans. Surjit tells Ivan that he would like to keep Rajbir as his beneficiary.

What should Ivan counsel his client to do?

- A. Surjit cannot make any changes to the policy without Rajbir's consent, as she is the irrevocable beneficiary of his policy.

- B. Surjit does not need to do anything as Rajbir is already the named beneficiary.

- C. Surjit should once again designate Rajbir as the beneficiary.

- D. Surjit should name a different beneficiary now that he is divorced.

正解:B

解説:

An irrevocable beneficiary designation remains valid even after a divorce unless the policyholder, with the irrevocable beneficiary's consent, decides to change it. As Surjit wishes to retain Rajbir as his irrevocable beneficiary, no additional steps are required. The designation's irrevocability ensures Rajbir's right to the policy benefits remains intact without needing re-confirmation. This complies with the provisions on irrevocable beneficiaries outlined in Quebec's Civil Code and reinforced by LLQP standards on irrevocable beneficiary designations.

質問 # 100

Insurance of persons advisor Somalia is careful to comply with the standards and regulations when she meets with potential clients. Under no circumstances would she want them to feel aggrieved or not respected. She makes sure to know their rights. Which legislation does Somalia not have to worry about?

- A. The Quebec Charter of Human Rights and Freedoms

- B. An Act respecting the distribution of financial products and services (Distribution Act)

- C. An Act respecting the protection of personal information in the private sector (APPIPS)

- D. The Insurers Act and the Regulation under the Act respecting insurance

正解:D

解説:

Comprehensive and Detailed In-Depth Explanation: Somalia, as an insurance of persons advisor in Quebec, must adhere to multiple legislative frameworks governing her professional conduct and client interactions.

The Distribution Act (option A) regulates her licensing, duties, and client dealings as a financial professional (Sections 1-12), making it directly applicable. The APPIPS (option B) governs how she handles clients' personal information, a critical aspect of her role (Sections 1-10), so she must comply. The Quebec Charter of Human Rights and Freedoms (option C) protects clients' rights to dignity and respect, influencing her ethical obligations (Sections 1-4). However, The Insurers Act and its Regulation (option D) primarily govern insurance companies' operations, solvency, and product offerings, not the day-to-day conduct of individual advisors like Somalia (Sections 1-20). While indirectly relevant through her insurer affiliations, it does not impose direct obligations on her client-facing duties. The Ethics and Professional Practice manual stresses advisors' responsibility to prioritize client-focused legislation, supporting option D as the least applicable.

References: Distribution Act, Sections 1-12; APPIPS, Sections 1-10; Quebec Charter, Sections 1-4; Insurers Act, Sections 1-20; Ethics and Professional Practice (Civil Law) Manual, Section on Legislative Compliance.

質問 # 101

Trisha is new to the insurance industry and wants to understand the primary responsibility of the Canadian Insurance Services Regulatory Organizations (CISRO). Which of the followingstatements about CISRO is CORRECT?

- A. To administer the regulatory system, applicable to insurance intermediaries.

- B. To provide clients with assistance to their enquiries and complaints pertaining to Canadian life and health insurance products and services.

- C. To administer the enforcement of the federal Personal Information Protection and Electronic Documents Act (PIPEDA).

- D. To help protect the integrity of the Canadian financial system.

正解:A

解説:

The primary responsibility of the Canadian Insurance Services Regulatory Organizations (CISRO) is to establish and maintain a cohesive regulatory framework for insurance intermediaries, ensuring consistent standards across provincial and territorial jurisdictions in Canada. CISRO does not directly interact with consumers or administer PIPEDA; rather, it collaborates with regional regulators to promote regulatory harmony for insurance professionals.

This responsibility helps uphold public trust and ensures that intermediaries comply with legal and professional standards.

質問 # 102

Aari and Jonila are a married couple in their late sixties. They both enjoy a comfortable retirement. Both receive regular payments from their pension plans, Old Age Security (OAS) and Canada Pension Plan (CPP).

They own a house and a cottage that are both mortgage-free. They also have over $500,000 in savings and investments. They know that if one of them dies, the surviving spouse will be financially comfortable. The couple has two grown children to whom they would like to leave all their assets when they die. The couple informs Herbert, their insurance agent, that they want to make sure when they die that their children have the funds needed to pay the taxes on the assets that they will bequeath them.

Which life insurance policy would be most suited to meet the couple's needs?

- A. A term joint last-to-die policy on Aari and Jonila.

- B. A permanent joint last-to-die policy on Aari and Jonila.

- C. A term joint first-to-die policy on Aari and Jonila.

- D. A permanent joint first-to-die policy on Aari and Jonila.

正解:B

解説:

AJoint Last-to-Die policyis designed to pay out upon the death of the second insured, which is beneficial for covering estate taxes. This structure aligns with Aari and Jonila's goal to provide funds for their children to pay taxes on inherited assets. Permanent coverage ensures the policy remains in force until both spouses have passed away, which supports long-term estate planning needs. First-to-die policies would pay out upon the death of the first insured, which would not align with their objective to have the policy available for estate settlement at the second death.Therefore,Option Ais most suitable.

質問 # 103

Sasha is an employee at PranaTech. The company offers all employees a pension plan. PranaTech must contribute into the plan, but employee contributions are not mandatory. Sasha chooses where his funds will be invested.

- A. Defined contribution pension plan.

- B. Defined benefit pension plan.

- C. Deferred profit sharing plan.

- D. Group registered retirement savings plan.

正解:A

質問 # 104

(Germaine, a shareholder-manager, already has a group RRSP for her employees. She now wants to establish a second group savings plan that allows employees to withdraw money at any time without additional taxes or penalties.

Which plan fits her needs?)

- A. ADBPP.

- B. APRPP.

- C. ADPSP.

- D. A group TFSA.

正解:D

解説:

Agroup TFSAallows employees to withdraw fundsat any time without triggering taxes or penalties, meeting Germaine's requirement perfectly.

Exact Extract:

"TFSAs allow contributions with after-tax dollars and withdrawals at any time without tax penalties, making them ideal for flexible saving plans." (Reference:Segfunds-E313-2020-12-7ED, Chapter 1.3.11.2 Group Plans)

質問 # 105

......

合格させるIFSE InstituteはPassTest試験問題集:https://www.passtest.jp/IFSE-Institute/LLQP-shiken.html

完全版最新のLLQP問題集で100%カバー率問題と解答があなたをリアル試験で合格させる:https://drive.google.com/open?id=1saeJJs67DXJQnIM3lLHmHRZ3tzn2vXyN